A hedge fund bankruptcy, SPAC's, Libor, Venmo and the LSE.

If you haven’t already, please do subscribe for a weekly newsletter, free of charge.

Follow us on Twitter: @banking_journal

The Week’s Briefing:

M&A

Nasdaq to sell US Treasuries trading business, eSpeed, to Tradeweb for $190m

Auto-insurance IT provider CCC Information Services to go public via SPAC in a $6.5 billion merger

Former British finance minister George Osborne joins boutique M&A investment bank Robey Warshaw - despite no experience in the M&A space.

Allianz to acquire full ownership of its China life insurance business, agreeing to buy the 49% that it did not already own.

Payments firm Payoneer Inc. to go public via Betsy Cohen’s SPAC for $3.3bn.

Mediobanca SpA’s credit fund Cairn Capital is to buy Blackstone-backed distressed debt fund, Bybrook Capital, adding $2.5bn to their AUM, boosting it to $8bn.

$28Bn-asset PacWest bought specialty real estate lender Civic Financial Services, with $4.4bn in RE loans, for an undisclosed amount.

Banking, Insurance & Regulation

Trading of Swiss shares in London restarted this week.

Hedge fund Greylock Capital files for Chapter-11 bankruptcy in NY after investors withdrew money en-masse after 3 years of losses - plans to lower costs and restructure its debt.

Nordea Bank to reorganize its $390bn wealth-management business.

FCA calls for full regulation of ‘buy now, pay later’ credit deals offered via fintechs, such as Paypal and Klarna, “as a matter of urgency”.

UBS to raise investment bank bonus pool by 20%

Ernst & Young estimates LIBOR transition to cost global global banks each $100MM this year, falling to $50MM in 2022.

Venmo’s debt-collection practices to be probed by the Consumer Financial Protection Bureau (CFPB).

German’s financial watchdog, BaFin, orders Goldman Sachs’ European division to comply with anti-money laundering rules to prevent money laundering and terrorist financing.

Point72 raies $1.5bn from investors, after losing 10% in January.

TD Bank combined its 2 lending groups to create a bigger commercial banking division

Citigroup’s new CEO, Jane Fraser, forms a new operating team to handle regulatory work in a bid to fix corporate governance issues, and the OCC and Federal Reserve, last year, warned them of failings with their technology infrastructure and internal controls.

Insurance & Bank Earnings

Prudential reports 27% YoY decline in profits, with Q4 profits coming in at $819MM (prev. $1.13bn). For FY 2020, they reported a loss of $374MM. AUM rose to $1.72 trillion, up from $1.55 trillion a year earlier. Plans to return $10bn to shareholders over the next 3 years through dividends and buybacks.

Deutsche Bank reported its first profit since 2014 after reporting strong investment banking and trading results in 2020.

Private equity firm, Apollo, reported net income of $434MM, up from $166MM a year before. Their PE portfolio gained 13% in 2020, almost beating the S&P 500.

Economics & Markets

U.S. annual trade deficit grows to its largest since the GFC.

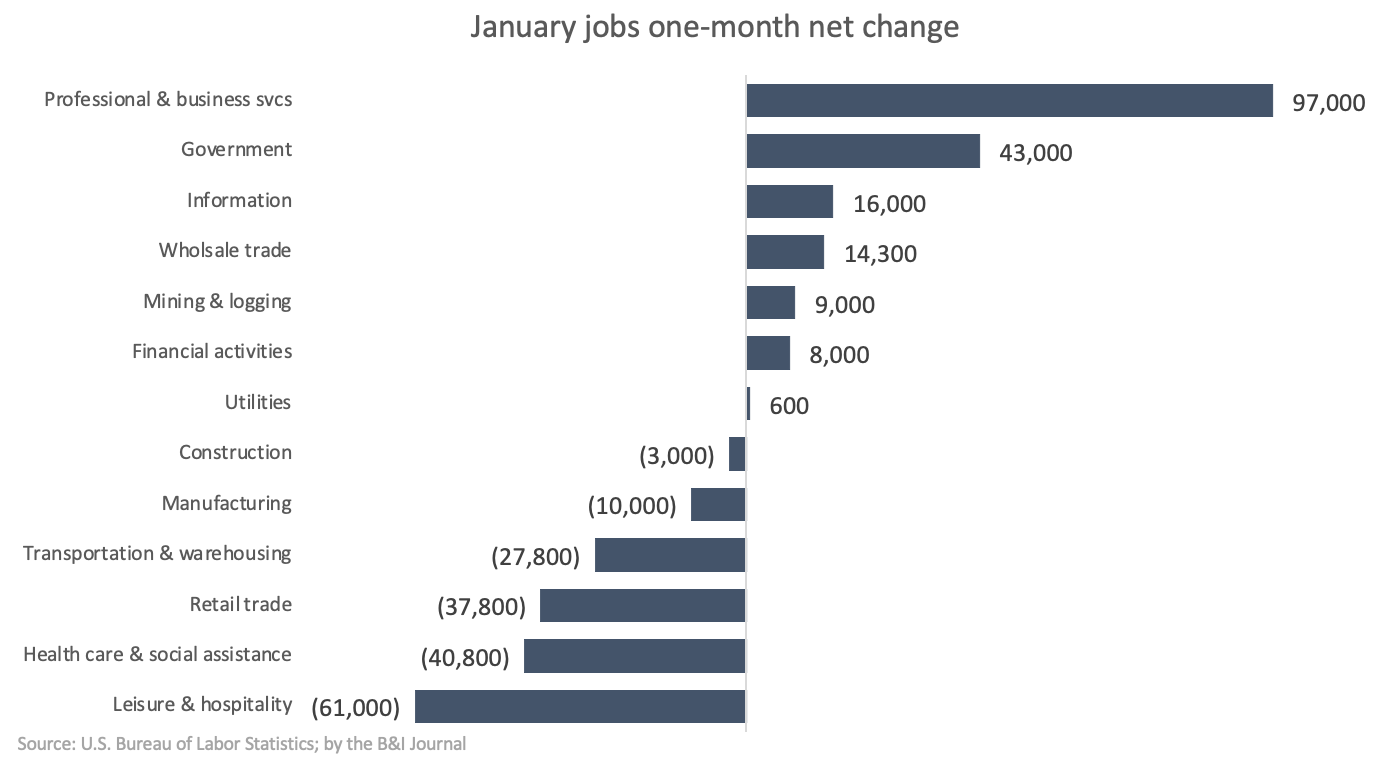

U.S. added just 49,000 jobs in January

U.K. house prices decline for the first time in 7 months

Euro zone Q4 GDP falls less than expected, still expected to contract in Q1.

Eurozone inflation turns positive for first time in 6 months in December - headline CPI came in at 0.9%, core-CPI was at 1.4%

Moody’s Analytics warns that US office rents won’t reach pre-pandemic rates until 2026, forecasting office vacancy rates will rise to 19.4%, a new high, this year. Office rents are projected to decline 7.5% for the year 2021.

Biggest stories of the week:

Trading of Swiss shares in London restarted this week

In 2019, Brussels stopped recognising that Swiss stock exchanges had equivalent supervisory regulation in a dispute over trade talks, banning trading of Swiss shares. As an EU-member, the UK had to comply, and overnight, 30% of the daily €4.5bn in Swiss trading left London for Zurich.

Exchange operators, such as SIX Group, LSE, and CBOE gladly welcomed the move, as no shares or francs are leaving Switzerland, yet the Swiss markets are more accessible to investors, their clients.

SIX Group, a Swiss exchange operator, said, despite it losing a little bit of market share:

“We have always been committed to open and international capital markets. This is in the interest of national and international investors and clients

With Turquoise and the other venues you’re getting a whole additional range of mechanisms to buy and sell, and that’s a net positive for investors.”

Although, whilst a cause for some optimism, the trading value of Swiss shares returning to London will not make up for the €8bn in daily transctions that left London for the EU after Brexit. It is a step in the right direction, but there’s still a long way for post-Brexit Britain to go in this industry. We will be talking more about Brexit next week.

Payments firm Payoneer Inc. to go public via Betsy Cohen’s SPAC for $3.3bn.

Payoneer Inc. is a profitable online payment firm used by large companies, such as Amazon and Airbnb. The company will go public via a merger with Betsy Cohen’s SPAC, FTAC Olympus Acquisition Corp. valuing Payoneer at $3.3bn. The transaction includes a $300MM PIPE (a private investment in the company).

Payoneer was founded in NY, in 2005, they say that the firm is profitable, and expect revenues of $432MM in 2021. The company allows e-commerce companies to send and receive money around the world, and processed $44bn in payments last year.

However, this is not the only similar kind of fintech-SPAC deal going on, recently a SPAC led by Bill Foley agreed to take Paysafe Group Ltd. public, and competes with a number of other public and private companies in the space.

Pro forma, the company will have about $563MM in cash

Their current shareholders will remain the largest shareholders in the firm

The deal is expected to close in H1 2021

Citigroup and Goldman led the SPAC, and Financial Technology Partners advised Payoneer.

Venmo’s debt-collection practices to be probed by the Consumer Financial Protection Bureau (CFPB)

In a regulatory filing by PayPal, they said that the CFPB is probing Venmo (a fintech, money-transfer service owned and operated by PayPal) into how the company treats customers who the company says owes them money for transactions that went wrong.

PayPal said they had received a “Civil Investigative Demand” from the CFPB “related to Venmo’s unauthorized funds transfers and collections processes, and related matters.” They said the CPFB has requested documents and answers to questions, and that PayPal is co-operating with regulators.

The probe is looking into claims that the company had threatened to send debt-collectors to users with overdrawn accounts, and even victims of scams.

The probe comes after the WSJ published articles last year and in 2019 about Venmo’s debt-collection practices.

Hedge fund Greylock Capital files for Chapter-11 bankruptcy

Emerging markets fund, Greylock Capital Associates filed for Chapter 11 bankruptcy protection in New York as investors withdrew large amounts from the fund following 3 consecutive years of losses.

The Chapter 11 will allow them to restructure their debt, lower costs and terminate its expensive Madison Avenue office lease in Manhattan.

Greylock has cut its staff from 21, three years ago, to just 9 people.

The fund’s AUM has more than halved since 2017, to a current $450MM at the end of 2020, and will drop by $100MM more by the end of Q1, if no more capital is injected into the fund.

Greylock was founded in 2004, and is led by Hans Humes, who is known for making investments in distressed debt and troubled sovereign bonds. Their fund negotiated the Greek government’s debt restructuring.

The fund came under significant pressure last year as emerging market bond prices nearly collapsed at the start of the pandemic, and creditors took losses in Ecuador and Argentina, and Venezuelan and Lebanese sovereign bonds also fell as the countries need to resolve their defaults.

Auto-insurance IT provider CCC Information Services to go public via SPAC

I suspect SPAC’s will frequently be a part of the newsletters, given their huge rise to popularity last year.

This one, I thought, was particularly interesting.

CCC Information Services Inc. is merging with thee SPAC Dragoneer Growth Opportunities Corp. to go public in a deal that values the company at $6.5 billion.

CCC allows policyholders to upload photos on their phone from an accident scene and, moments later, get a repair estimate via artificial intelligence.

The company’s clients include 300 insurers, 25,000 auto-repair facilities, dozens of car makers and thousands of parts suppliers.

It will raise $1bn together, with $690MM from the blank-check merger, and the rest coming from the PIPE.

The funds raised will be used for R&D, towards artificial intelligence and machine learning to speed up and improve the estimated claims valuation.

Its competitors include Alphabet’s Google Cloud unit, working with insurance firm, USAA, which is developing a similar photo-based estimating program for USAA’s policyholders.

Another is a London-based tech startup, Tractable, which has partnered with Hartford Financial Services Group Inc. to develop similar technology, working with a CCC rival, Mitchell International Inc.

Investors in CCC include, Mike Bloomberg’s family office, Willett Advisors, as well as mutual funds, such as T. Rowe Price, and Fidelity.

The company will be renamed CCC Intelligent Solutions Holdings Inc. and will start trading on the NYSE when the deal closes in Q2.

General Market & Economic Observations

Economic summary:

Total nonfarm payroll employment rose by 49,000 last month - a very weak start to the year

Even more concerning data from the jobs report was that 39.5% out of the unemployed were out of work for 27 weeks or more. This rose MoM, and is nearing a record peak that was set in 2010. This signals a huge rise in long-term unemployment, which is very concerning for a healthy economic recovery.

Manufacturing was slightly weaker, but still strong in January, with the PMI coming in at 58.7%

The USD rose last week, yields also rose slightly, the back end of the curve steepened, and 5 year breakevens near 2011 highs, well above the FED’s 2% inflation target.

The BoE expects a strong vaccine-induced economic recovering in the second of the year, but still expect a 4% decline in GDP for Q1

They also said they would force commercial banks to prepare for negative interest rates to be imposed in six months. However, they made clear that this was not a sign that the BoE’s Monetary Policy Committee thought such a move was necessary.

The BoE’s policy statement led to the pound strengthening against the dollar by 0.8%, and a sell off in government bonds, leading to interest rates rising by 4 bps.

They will complete £150 billion of additional QE for 2021, trying to keep inflation near its target 2%.

Today’s Discussion:

LIBOR

For 50 years, the LIBOR has been used to determine the cost of borrowing around the world. It is derived from a daily survey of bankers who estimate how much they would charge to lend to counterparties. It was simple, ubiquitous, effective, and, supposed to be, reliable.

Libor is used to set interest rates for all kinds of derivative contracts and financial assets, such as: floating-rate notes, CLO’s, complex derivatives, mortgages, student loans, and credit card rates.

However, in 2008 regulators found that the banks had been manipulating the rates to their advantage.

The value of financial contracts linked to LIBOR are currently estimated to be ~$240 trillion.

In 11 months, 5 currencies - the U.S., Switzerland, U.K., euro zone, and Japan - will officinally discontinue the LIBOR rates. Many countries are creating their own alternative benchmarks to Libor.

Investors, and corporate treasurers have to re-write all financial contracts linked to Libor, to stop deals turning into a chaotic mess, and bankers have to re-develop financial softwares and adjust their portfolios for the transition.

Most Libor rates will be phased out at the end of this year, although banks have urged regulators to delay the timeline to mid-2023, to give time to abandon the Libor benchmark.

The FED and other regulators have urged banks to stop new Libor-issuance, due to “safety and soundness risks” - they signalled that market participants should stop issuing USD Libor-based contracts and instruments, and use SOFR to write new ones.

So, what are the benchmarks that will replace LIBOR?

In the U.S., SOFR will be adopted in Libor’s place. It is different to Libor in three ways:

- It will not be set by bank quotes, it will instead be based on actual transactions.

- SOFR provides only an overnight rate, unlike Libor, which offers rates for 7 maturities ranging from 1 day to a year

- SOFR is a secured rate, which is derived from repurchase agreement transactions, collateralized by U.S. Treasuries.

In the Eurozone:

Euribor - it currently underpins more than $211 trillions of assets. It has long been used in favour of Libor in Europe.

In the U.K.:

The ‘Sterling Overnight Index Average’ (Sonia). It has been in use since 1997. It measures the rate paid on unsecured overnight funds and includes transactions negotiated between banks, and broker-intermediated loans. It is curreently used to value ~£30bn of trades a year. Sonia is now about the same size in the GBP-swaps market as Libor.

Switzerland:

The Swiss Average Rate Overnight (Saron). It is very similar to SOFR - Saron is based on transactions between financial institutions. Mortgages in Switzerland are being offered using Saron, although a majority of the credit markets are still based on Libor.

Why is the Libor transition so important?

Due to the vast size of the LIBOR market, with hundreds of trillions of dollars linked globally to it, it is likely to be the most important development in the financial markets, ever.

Although, Libor replacements are still vulnerable to manipulation, for example in Tokyo, they recently had a similar scandal to one of Libor’s expected replacements in Japan. And just a few years ago, a number of traders were charged attempting to manipulate to Euribor.

How was Libor manipulated?

As Libor was set by bankers, traders and borrowers bribed (with dinners, pleading and even begging) their counterparts at other banks (even their own) who were in charge of submitting daily estimates of IBOR (interbank offering rates) to the official Libor calculation process. They used this to lock in lower rates (low rates were seen as a sign of strength during/before the financial crisis) and adjust the benchmark to help their open positions.

Over $9 billion in fines were paid by banks in the rigging scandal (see the chart by the FT below).

The current estimated transition costs per bank are $100MM this year, and another $100MM over the next two years.

Thank you for reading!

If you enjoyed it, please subscribe, and stay tuned for next week's newsletter.

Also, do share this with others, and if you would like to contact me with any feedback, please do, at:

Email: BIJournal@outlook.com

Twitter: @oabdelmaged1

Twitter: @banking_journal

Disclaimer: This content is for informational purposes only, it does not contain or offer investment advice, and it should not be treated as such. You should not construe any such information as financial, investment or any other advice. I/we may, directly or indirectly, have positions in securities mentioned on this site. I am (/we are) not registered as financial, or investment advisors, or securities broker-dealers with the Securities and Exchange Commission, FINRA, or any other securities regulatory body or authority. All materials and information presented on this site are believed to be true and accurate, however we cannot guarantee that they are. The materials on this site also represent the views of the writer, and their opinion, and do not represent the opinion of those associated with the writer. Use the materials and information presented on this site, and newsletter at your own risk. Any views or opinions are not intended to malign any institution, organization, company or individual. By reading and/or using any information and/or content/material on our site, and/or this newsletter, you accept and agree to our disclaimer.