Brexit, the FED, and the NYSE

If you haven’t already, please do subscribe for our weekly newsletter.

Follow us on Twitter: @banking_journal

The Week’s Briefing:

M&A

Fintech firm OppFi to go public via SPAC, merging with FG New America Acquisition Corp.

Banking, Insurance & Regulation

NYSE threatens leaving New York over proposed stock transfer tax laws

Germany’s first privatized bank Landesbank plans major acquisitions

Citadel CEO Kenneth Griffin to testify to the House Financial Services Committee, Thursday, regarding Gamestop

The BOE plans to toughen rules on banks in first major post-Brexit regulatory proposal

FED to stress-test banks’ ability to withstand 55% decline in equity prices

Greece’s third-largest lender, Piraeus Bank SA, plans to raise $1.2bn in capital, to dilute the government’s state fund’s stake from 61.3% to 30%

Hong Kong stock exchange hires JPMorgan banker for its Chief Executive role

US stock exchanges (the NYSE & Nasdaq) sue the SEC over new data rule changes

FHFA announced new plans to further aid mortgage borrowers

Insurance & Bank Earnings

Fannie Mae’s FY 2020 earnings fell due to Covid-related expenses. FNMA reported Q4 net income of $4.6bn, up from $4.2bn in Q3 and $4.4bn a year earlier. Quarterly profits were boosted thanks to low interest rates, and a housing boom. FY’20 earnings were $11.8bn, down from $14.2bn in 2019

A number of European banks reported earnings last week, and quite frankly they were nearly all bad, and many resulted in long term dividend cuts (such as Commerzbank). I won’t waste your time on them.

Economics & Markets

U.S. 30-year treasuries sell off reaching a 2% yield for the first time since the pandemic began

Bank stocks rallied slightly on the back of higher yields

The U.K.’s economy grew more-than-expected in Q4, up 1.5% - the U.K.’s GDP contracted 9.9% in 2020, the most in 300 years

Treasury secretary Janet Yellen urges global finance ministers at the G7 to go big on stimulus and support for the global economy

Janet Yellen predicts full U.S. employment next year if $1.9tn stimulus package is passed

FY 2020 and Q4 2020 U.S. CPI data showed no sign of inflation

So-called ‘Buffett-indicator’ - which measures the stock market cap to the GDP - reached a record high of ~228% of GDP this week. Far eclipsing the ~179% at the height of the dot-com bubble

The Bitcoin bubble continues to inflate, with prices nearing $50,000

Biggest stories of the week:

US stock exchanges (the NYSE & Nasdaq) sue the SEC over new data rule changes

The New York Stock Exchange, Nasdaq and CBOE Global Markets have sued regulators (the SEC) over new rules that would force them to share more data in an effort to increase competition in the sector.

The SEC said it wanted to help more investors get high-quality data at faster speeds, but the exchanges have argued the rules could undermine their proprietary data businesses, which offer premium data services to paying users.

The lawsuits were filed in an effort to block the rules from being implemented on the grounds that the SEC has overstepped its authority.

The data rules were announced last year after a unanimous vote at the commission.

Allison Lee, now the acting chair of the commission, accused the 3 exchanges of offering some customers “a pricey trip along a freshly paved, proprietary high-speed toll lane” and others “a cheaper ride on a public highway with cracked pavement and potholes”.

New FED stress-test scenario’s released

The Federal Reserve will test bank’s ability to withstand a 55% decline in equity market prices, and a hypothetical scenario under which unemployment would jump to above 10% and markets seize up, as well as “substantial stress” in commercial real estate and corporate credit markets

Under a “severely adverse” scenario, unemployment would rise 4pp to 10.75% in Q3 of next year, the GDP would decline and asset prices sharply drop, with equity markets falling 55%.

The Vice Chair for Supervision, Randal Quarles said:

"The banking sector has provided critical support to the economic recovery over the past year

Although uncertainty remains, this stress test will give the public additional information on its resilience.”

The baseline scenario for 2021 is in line with current economic projections that forecast a decline in unemployment, stable inflation and steady expansion in international economic activity. Both the baseline and the severely adverse scenario contain 28 variables, including interest rates, stock market prices and gross domestic product.

Banks are required to submit their capital plans to the Fed by April 6.

The FED’s bank stress test was introduced after the GFC to test the banking systems ability to withstand a severe economic downturn. It tests whether a bank has sufficient capital to weather economic crises, as well as whether they can also make 4 quarters of shareholder dividend payouts.

To return capital to shareholders, through buybacks and dividends, the banks must pass the stress tests.

FHFA announced new plans to further aid mortgage borrowers

The FHFA will allow mortgage borrowers with loans backed by Fannie Mae and Freddie Mac to request an additional 3 months of forbearance.

The Coronavirus Aid, Relief and Economic Security Act passed by Congress last year allowed borrowers with fed-backed mortgages to request up to 12 months of forbearance if they were financial affected by COVID-19.

As of February 28th, borrowers under that plan can request an additional 3 months of forbearance - giving them coverage up to 15 months.

They will also extend their moratorium on single-family home foreclosures until March 31 “to keep families in their home during the pandemic,” - FHFA director, Mark Calabria said.

President Biden is asking Congress to allow borrowers to request forbearance through September 30 in his new stimulus package, which would also ask for the national foreclosure and eviction moratorium on fed-backed mortgages to be extended until the end of September.

The BOE plans to toughen rules on banks in first major post-Brexit regulatory proposal

In the BOE’s first major post-Brexit regulatory proposal, regulators will impose a tougher rule on British banks than if the U.K. was still a part of the EU.

The BOE’s Prudential Regulation Authority (PRA) said that it will not allow lenders to get a capital benefit from their investments in software technology. This is very different to the EU, which last year allowed its lenders to get a break on capital worth up to 20bn euros.

The PRA says that the EU’s decision would harm the safety of British banks as it would leave them with less capital and few resources to absorb losses on loans or trades that go bad.

The BOE’s proposal also includes a wide-ranging regulatory proposal which implements international capital and liquidity standards. The BOE also said that it will complete a review of restrictions on bank leverage by the middle of the year.

This comes at a time of heightened political tension between the EU and the U.K. who are in major disagreement over a financial trade deal for Brexit, where neither side will agree to each other’s proposals. The EU has said that it will not grant the EU easy access to London’s financial markets unless they can scrutinize all of the UK’s regulatory plans incase they dampen down standards.

General Market & Economic Observations

There were no major economic data releases this week, except for:

Core CPI (Jan): 0%

CPI (Jan): 0.3%

Initial jobless claims (Week Feb. 6): 793k - prev. 812k

Continuing claims (Week Jan. 30): 4550k - prev. 4690k

Inflation expectations continue to rise

The KBW bank index nears reaching pre-pandemic highs

The UK’s GDP contracted 9.9% last year, the most in 300 years - the BOE expects a sharp and very strong recovery in the second half from rapid vaccine deployment

U.S. junk bond yields fall below 4% for the first time ever - CCC bond yields fell to 6.21%, single-B issues yielded 4.3%, and BB’s yielded 3.05%

Today’s Discussion: Brexit

The U.K. financial services industry left the EU with a no-deal. It was completely ignored by the government leading up to Brexit in favor of things like fishing, and as a result was omitted from the last-minute deal.

The U.K. once had a near global monopoly when it came to things like derivatives trading, and especially share trading within Europe.

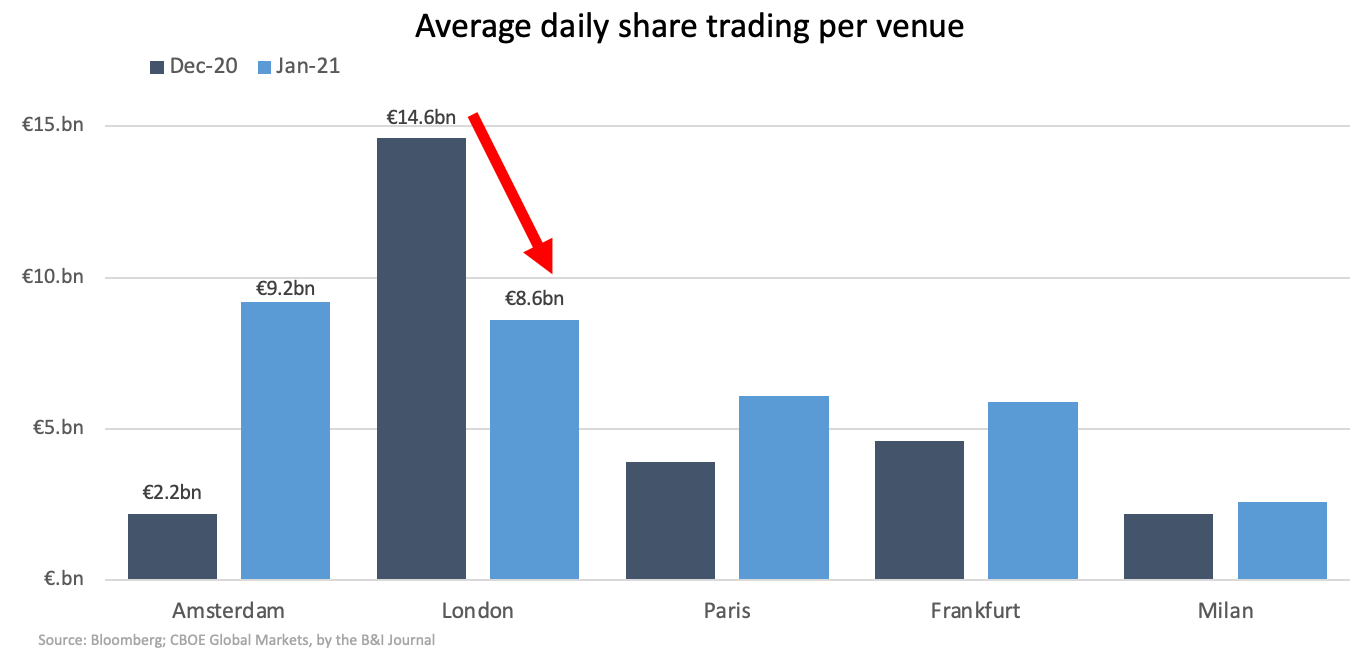

Trading in Euro-denominated swaps, a $1.6 trillion-a-day market, started leaving London in December, and, as shown in the chart above, was taken over by the EU and the US.

This week, Amsterdam overtook London in daily shares trading, which is a symbol of London losing its once dominant position in European financial markets. This does not account for Swiss shares trading in London, which recently restarted. That will slightly make up for the trading losses to the EU.

Although, there are some ambitious plans for London’s future, one being making the UK a global hub for green finance. However, Intercontinental Exchange (ICE) just said that it will transfer the EU’s €1bn-a-day carbon emissions trading market from London to the Netherlands - clearing will remain in London.

Many jobs have left London for the EU, and job openings have declined significantly since the Brexit vote:

Whilst trading for some securities left rapidly from the UK, many bankers and asset managers are less pessimistic about London’s future, such as Barclays’ CEO, Jes Stanley, who is much more upbeat about the situation, believes that the government should focus less on the EU, and focus more on global financial hubs - he strongly believes that London will become a global hub for green finance in the future:

“There are some jobs that are going to Europe, that otherwise would have been in the U.K., but it’s in the hundreds, Barclays employs some 50,000 people in the United Kingdom, roughly 20,000 outside of the UK and 10,000 in the US.

Some amount of capital has moved but London is still obviously the main center for Barclays.

What London needs to be focused on is not Frankfurt or not Paris, [it] needs to be focused on New York and Singapore.”

He also said that deregulation was not the answer for London to maintain its competitiveness as a financial hub, as regulation “protects the financial industry.”

Asset managers and hedge funds have hardly left London and are not expected to shift operations or assets from London in the future.

Much of the recent changes in the market were driven by a stand off between London and Brussels, unable to reach a deal - as each side wants to assert their own regulatory supervision. Both sides say the most actively traded swap contracts should be traded on venues they both accept as having an “equivalent” standard.

As a result of there being no agreement, EU banks routed most trading and deals through the US, whose standards are accepted on both sides. A deal between Brussels and London would greatly reduce friction and fragmentation in the markets.

The BOE’s governor, Andrew Bailey, said that the EU’s post-Brexit requirements to grant access to markets unrealistic.

“The EU has argued it must better understand how the U.K. intends to amend or alter the rules going forwards.

This is a standard that the EU holds no other country to and would, I suspect, not agree to be held to itself.”

Without an equivalence deal, London-based firms wishing to operate also in the EU are left indefinitely with the additional costs and complexity of supporting operations in both places.

The 3 areas where the U.K. is looking at diverging from EU regulations are:

No longer applying Basel rules to small banks that aren’t internationally active

Excluding software assets from measurements of bank capital

Review Solvency II rules for life insurers.

The EU is concerned that Brexit is a way for London’s financial markets to be deregulated and become less stable. Bailey addressed these concerns as well:

“None of this means that the U.K. should or will create a low-regulation, high-risk, anything-goes financial center and system,”

So, will Brexit bring an end to the UK’s once-dominant financial services industry?

Whilst the effects so far are looking severe, and there are many doomsayers calling London finished, I don’t believe that London is over. The old London may never be seen again, but Brexit was an opportunity for the UK to reinvent itself, as it has many times before. London has at least one benefit that no-one can take away from them, that’s it’s convenient physical location, between Asian, U.S and European trading hours.

Efforts are already being made to make London’s financial markets more attractive, such as Stock Exchange-listing reform, to make it more attractive to tech startups. SPAC-listing rules are also being redone. And a strong effort is being made to make London a hub for green finance.

Brexit also allows London to compete globally with Singapore and the U.S., and focus less on the EU.

Although, the negative effects cannot be ignored. Amsterdam has taken over London in shares trading, derivatives trading has left the UK en-masse over uncertainty. Jobs and assets have shifted to the EU. Maybe, as more trading moves to the EU, more will follow - thanks to a world of almost decentralized and computerized trading.

The future of London depends really on how the government acts, and so far, they have not acted in a promising way - with Boris’ government almost ignoring the financial services sector as a whole.

What we’re reading:

Dan Loeb’s Third Point’s Q4 2020 Investor Letter

FT: Muddy Water’s Carson Block on market flows and bubbles in a piece for the FT

Bloomberg: “Mario Draghi Puts Italy at the Grown-Ups' Table”

Bloomberg: “The Road From Brexit to Becoming a Settled State”

NYT, Andrew Ross Sorkin on SPACs: “Wall Street’s New Favorite Deal Trend Has Issues”

Thank you for reading!

If you enjoyed it, please subscribe, and stay tuned for next week's newsletter.

Also, do share this with others, and if you would like to contact me with any feedback, please do, at:

Email: BIJournal@outlook.com

Twitter: @oabdelmaged1

Twitter: @banking_journal

Disclaimer: This content is for informational purposes only, it does not contain or offer investment advice, and it should not be treated as such. I/we may, directly or indirectly, have positions in securities mentioned on this site. I am (/we are) not registered as financial, or investment advisors, or securities broker-dealers with the SEC, FINRA, or any other securities regulatory body. All materials and information presented on this site are believed to be true and accurate, however we cannot guarantee that they are. The materials on this site also represent the views of the writer, and their opinion, and do not represent the opinion of those associated with the writer. Use the materials and information presented on this site, and newsletter at your own risk. By reading and/or using any information and/or content/material on our site, and/or this newsletter, you accept and agree to our disclaimer.